Editor's note: With the dual incentives of policies and markets, the LCD panel market in Mainland China has become a global highlight. Domestic companies including BOE, TCL, and Dragon Optical have all launched high-end LCD panel production lines, but this concentrated investment also brings There are too many investment entities and other market risks.

What is the status of the LCD panel industry in China? The reporter recently analyzed the equity structure and technical reserves of the three high-generation LCD panel production line companies of BOE, TCL, and Longteng Optoelectronics to reflect the overall layout of China's LCD panel industry.

Capital: Integration is the Best Way to Solve Problems

For the funding of the LCD panel production line, Zhang Yu, director of BOE Public Relations, told the China Electronics News: “As we all know, LCD panel production lines have invested a lot. For investment in the LCD panel industry, which has a billion-dollar investment, the capital has always been the main obstacle to the development of the industry. In particular, due to the influence of the liquid crystal panel industry's development law, the outside world is also worried about the company’s huge investment in the liquid crystal panel industry. In fact, in the early stage of the industrial downturn and the development of the industry, insisting on or even expanding the investment may make China The electronic information industry has achieved leap-forward development. In solving the financial difficulties, in addition to market financing, the introduction of venture capital, the cooperation of upstream and downstream manufacturers, the support of relevant national policies is also very important."

Obviously, funding is a common problem faced by companies entering the LCD panel industry. At present, BOE 8.5th Generation Line, Longteng Optoelectronics 7.5th Generation Line and Huaxing Optoelectronics 8.5th Generation Line have been approved by the National Development and Reform Commission.

BOE's panel production lines are all run as project companies and are all subsidiaries of BOE Group. Its 5th generation LCD panel production line is 82.49% controlled by BOE Group, and BOE Technology Group's share of the 4.5th generation LCD panel production line is 98.7%. The 6th generation LCD panel production line BOE Group holds 100% shares and the 8.5th generation under construction. The liquid crystal panel production line will also adopt the equity model similar to the above project company. "In terms of financing plans, the company plans to raise 10 billion yuan in the form of a private placement. Among them, it is planned to use 8.5 billion yuan to raise funds for the construction of the 8.5th generation line, and another 1.5 billion yuan to supplement the working capital." Zhang Yu told reporters.

Huaxing Opto-electronics' 8.5th generation panel production line project has a total investment of 24.5 billion yuan and a capital of 10 billion yuan, and Shenzhen Chao and TCL each shoulder 5 billion yuan. He Chengming, general manager of China Star Optoelectronics Technology Co., Ltd., and Vice President of TCL Group He Chengming told the China Electronics News reporter: “Based on the principle of openness, Huaxing Optoelectronics will introduce other color TV manufacturers and related manufacturers as strategic partners to introduce more manufacturers in the future. Participate in the project."

Longteng Optoelectronics chose to develop in Kunshan. There are two reasons: First, the government of Kunshan invested 51%, and the government and the company share risks. The second is that the upstream manufacturers' support for Dragon Optical is in place. It is understood that the Kunshan municipal government is very active and not only builds an optoelectronic industrial park, but also earnestly considers enterprises and introduces supporting enterprises. Kunshan Longteng Optoelectronics Co., Ltd. general manager and chief executive Lu Boyan said: "To succeed, we must also have the cooperation of the industrial chain, must have competitive financing channels, and must have continuous investment."

Taken together, the high-generation LCD panel project that has already been launched still has the problem of shortage of funds. In particular, the follow-up capital investment will become the biggest problem.

Reporter Comments

It should be said that the current problem with LCD panels is not the issue of overcapacity, but the excessive number of subjects. Too many entities mean that the funds are scattered and cannot form a joint force. The mutual integration between enterprises may be the best means to ease the financial pressure. At this time, the government's support and guidance are particularly important.

Under the background of too many entities, especially Japanese and Korean panel companies have accelerated the production of LCD panel production lines of the 6th generation and above in mainland China, the government authorities should formulate a LCD panel industry development strategy that suits China’s national conditions and increase To support policy support for local enterprises, create an industrial atmosphere suitable for the development of Chinese enterprises, and concentrate on supporting leading enterprises with technological foundation and independent innovation capabilities, so as to become bigger and stronger Chinese LCD panel industry.

Technology: Build China's Characteristic LCD Panel Industry

BOE, Longteng Optoelectronics and TCL are companies that have been approved by the National Development and Reform Commission to develop high-generation LCD panel production lines. As the first group of companies in mainland China involved in high-end LCD panel production lines, their technical autonomy is a topic of concern.

The reporter learned that these companies have accumulated many aspects before they set foot in the advanced generation line. “We have already acted in talent development. At the beginning of building the factory in Kunshan, Longteng Optoelectronics took advantage of the talent gathered in the Yangtze River Delta region and continuously attracted talented people.†Lu Boxan told the “China Electronics News†reporter.

TCL Group and Shenzhen Shenchao Co., Ltd. recently cooperated to establish Huaxing Optoelectronics Technology Co., Ltd. to produce the 8.5th generation LCD panel. The company also focuses on the talent strategy. It is understood that by recruiting technicians from the world's major LCD panel makers, Huaxing Optoelectronics now has a stable group of technical experts.

BOE is taking the M&A route. According to Zhang Yu, director of public relations of BOE, after 8 years of investigation and demonstration preparation, BOE entered the liquid crystal display industry with its core technology in overseas mergers and acquisitions, thus mastering the core technology of LCD panels. Currently BOE's super edge electric field conversion technology is one of the two representative technologies in the industry.

Patents are the key indicators to measure whether a company has mastered the core technology in this field. It is understood that currently there are nearly 5,000 patented technologies that can be used by BOE, and more than 300 new patents are applied every year. Since the establishment of the company, Longteng Optoelectronics has applied for more than one hundred patents for inventions at home and abroad with independent innovation in just a few short years. At the same time, Longteng has developed a number of desktop monitors, notebook computers and LCD TV panels.

The relevant person in charge of China Star Optoelectronics told reporters that in today's high-generation production line technology, building technology, process technology and product technology are the three major technologies. Among them, the plant construction technology is very mature and can be solved by the engineering design institutes and construction units; most of the process technology has been solidified in the process equipment and can be provided by the equipment manufacturers; in terms of product technology, the company has independently developed and cooperated It is difficult to realize the technologies in development, design, manufacturing and other aspects.

On the basis of the development of existing technologies, these enterprises also made more preparations for future technological development. BOE began construction of the National Engineering Laboratory for Liquid Crystal Panel Process Technology in April 2009. This is China's first and only state-level national engineering laboratory for liquid crystal panel process technology. The laboratory is an independent development and operation of the State Development and Reform Commission relying on BOE, which reflects the country's recognition of BOE's technological strength and innovation in the LCD panel industry.

Lu Boyan revealed that the Dragon Optical Flat Panel Display Technology Institute was officially unveiled in 2008 and is expected to be completed this year. The company's work goal for 2011-2015 is to increase investment in LCD panel R&D on the basis of the original, and to accumulate technology from the senior generation line.

Reporter Comments

Having the core technological advantage is the basis for companies to establish a foothold in the panel industry. Overall, the overall strength of BOE, TCL, and Longteng Optoelectronics in the field of LCD panels is not as good as that of Samsung, Sharp, and other international first-tier panel makers. However, they have achieved a combination of independent innovation and technology research and development and have made Chinese characteristics.

However, judging from the technological reserves required for the development of the LCD panel industry, the technical voice of LCD panel companies in mainland China is still weak. Some companies choose to set up joint venture companies to obtain technical licenses and introduce technical teams to solve the technical bottleneck. Objectively, this is an emergency method. The growth of the panel industry in mainland China also requires companies to further strengthen their own technological reserves and enhance their management and operation capabilities.

Of course, in the development of the LCD panel industry in mainland China, on the one hand, Chinese companies must have independent technologies and highlight Chinese characteristics. On the other hand, the departments responsible for the development of the industry should also play a role of government guidance and subjective initiative in corporate participation. For enterprises with technological foundations and development prospects, the competent government departments should give policy and financial support, and at the same time concentrate resources on the development of high-end panel production lines in mainland China to enhance the company's basic research and independent research and development capabilities, and avoid redundant and disorderly construction.

Market: Need to increase resistance to risk

"Now there are few LCD panel production lines, and it is too early to discuss the issue of overcapacity." Compared with the second half of last year, the interviewees are now more sensible.

He Chengming stated that the development of the LCD industry is a cycle, and the market demand is fluctuating. However, in the next few years, the demand for LCD TVs will grow by a large margin. From the panel supply market forecast, the global production capacity can reach an annual output of 150 million LCD TV panels. By 2013, the global LCD TV market demand will be 203 million units. Considering the inventory of circulation, it will require about 220 million panels. If all the projects to be built in China are launched, it is estimated that in 2013, there will be more than 80 million LCD TV panels in China, which is estimated to be 40% of the global total. matched.

Zhang Yu told reporters that from the demand point of view, by 2012, the global shipments of LCD TVs will be 186 million units, and the market share will reach 76.5%. Among them, 30-inch LCD TV shipments were the largest, accounting for about 43% of all LCD TVs. Most of the above data is the demand for replacing CRT (CRT) TVs, and due to the flat panel display characteristics, new demands are still expanding, so whether the market will appear to be oversupply depends on the demand situation.

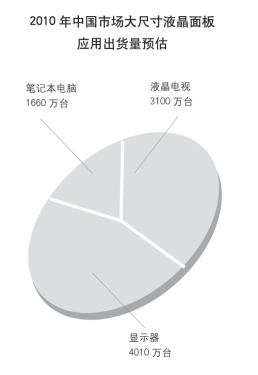

According to DisplaySearch's forecast, in the LCD product market in mainland China, the estimated demand for notebook computers in 2012 will be 51.69 million units with an amount of USD 27.6 billion; the estimated demand for monitors in 2012 will be 56.79 million units with an amount of USD 6.6 billion; TV 2012 The estimated demand is 47 million units and the amount is 16.6 billion US dollars. In the global LCD product market, notebook computers are expected to have a demand of 222 million units in 2012, with a total amount of USD 123.9 billion. The monitor is expected to have a demand of 203 million units in 2012, with an amount of USD 23.8 billion; TV's estimated demand in 2012 will be 221 million. Taiwan, amounting to 81.8 billion U.S. dollars. From this perspective, there will be no excess capacity.

However, the reporter found that the market's improvement does not mean that the pressure on mainland China's panel companies is decreasing. According to statistics, by the end of last year, the total annual production capacity of the 8th generation and above panel production line has reached 6.74 million pieces, of which the 8th generation annual capacity of Samsung Electronics reached 2.04 million pieces, and Sharp's 10th generation line production capacity reached 4.5. Millions. These do not include the production capacity of the 8th generation line that Chi Mei is currently constructing and the 8th generation line that LGD plans to expand. In addition, Japanese and Korean companies represented by Sharp, Samsung, etc. are planning the construction of higher-generation panel production lines such as 11th-generation line and 12th-generation line. The high-generation LCD panel project being established in mainland China must fully consider the risk of capacity saturation and increased competition.

Reporter Comments

If any industry develops blindly without restriction, it will cause waste of resources and impact on the normal market order. This is not a good thing for the country’s economic development.

The LCD panel industry is like this. Driven by huge profits, no company is willing to give up this "sweet cake." The inland panel enterprises supported by countries such as BOE, Longteng Optoelectronics, and China Star Optoelectronics should further broaden their vision of the industry, take a broad view of the international market, and launch multi-channel market competition.

Of course, from the market point of view, the phenomenon of oversupply in the short term is unavoidable, but China's LCD panel companies must have the ability to balance the global market, so as to form the core competitiveness.

Pond Fountain Pumps,Fountain Pump,Pond Water Pumps,Electric Fountain Pump

Sensen Group Co., Ltd.  , https://www.sunsunglobal.com