From a global perspective, the leading countries in artificial intelligence are mainly the United States, China and other developed countries.

Artificial intelligence is the most important technological social change that human beings face today. From national governments to capital and industry, they embraced artificial intelligence. In this context, it is necessary to know where the barriers to technology are and to understand where the boundaries of commercialization are, in order to better understand artificial intelligence. Recently, Tencent Research Institute issued the "China and the United States artificial intelligence industry development report." The reporter extracted and interpreted this.

From a global perspective, the leading countries in artificial intelligence mainly include the United States and China. Therefore, it is very important to understand and be familiar with the maturity and shortcomings in the industry. This report is very solid, authoritative data source, from the upstream and downstream to sort out the similarities and differences between the Chinese and American artificial intelligence industry, the gap, citing a large number of cases for analysis and interpretation, a text knows the layout of China and the United States.

The following is the report content:

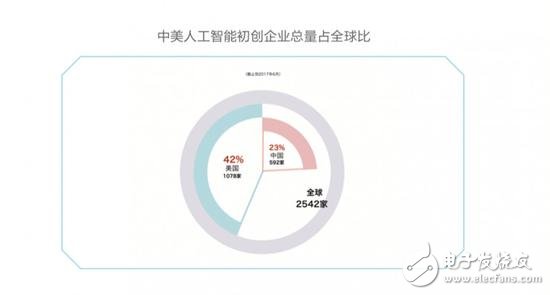

From a global perspective, the leading countries in artificial intelligence are mainly the United States, China and other developed countries. As of June 2017, the total number of artificial intelligence companies worldwide reached 2,542, of which 1078 were in the United States, accounting for 42%; followed by China, with 592, accounting for 23%. There are 486 differences between China and the United States. The remaining 872 companies are located in Sweden, Singapore, Japan, the United Kingdom, Australia, Israel, India and other countries.

From the existing statistics, the American artificial intelligence enterprise was founded in 1991, from 1991 to 1997, after the germination period, from 1998 to 2004, the development period, and from 2005 to 2013, the high-speed growth period. It has entered a stable phase since 2013.

Compared with the United States, China's AI industry progressed slightly later. It started in 1996, entered the development period in 2003, and entered the period of rapid growth from 2008 to 2015. By 2015, there were 166 enterprises related to artificial intelligence.

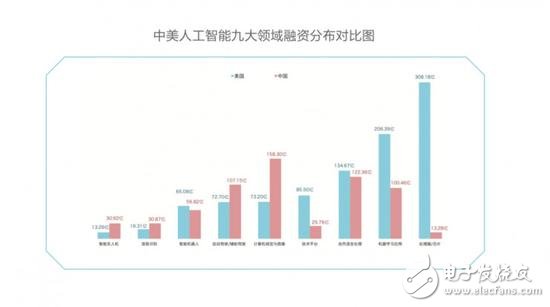

Sino-US AI venture capital financing comparison

If technology is blessed by capital, it will promote the landing and progress of technology.

The layout of the AI ​​industry in the United States is very complete. The basic layer, the technical layer and the application layer are involved, especially in the core areas of algorithms, chips and data, which have accumulated strong technological innovation advantages. The number of enterprises at all levels is leading China. In comparison, China has a large gap in basic components and basic processes.

Judging from the number of chip companies at the base level, China has 14 companies, 33 in the United States, and China is only 42% in the United States. At the technical level, there are 273 in China, 586 in the United States, and 46% in China. At the application level, there are 304 companies in China, 488 in the US, and 62.3% in China.

Overall, the United States is leading China in terms of the number of enterprises. The number of enterprises at the basic and technical levels is about twice that of China, but at the application level, the gap between China and the United States is slightly smaller.

Chinese investors are paying more attention at the application level. Among the Chinese artificial intelligence enterprises, the top three areas of financing accounted for computer vision and image, financing 14.3 billion yuan, accounting for 23%; natural voice processing, financing 12.2 billion yuan, accounting for 19%; and autonomous driving / assisted driving Financing 10.7 billion yuan, accounting for 18%. It is worth mentioning that although there are only 31 autopilot/assisted driving companies in China, the financing amount is the third, indicating that Chinese investors are very optimistic about this field.

US investors are more concerned about the foundation. Among the US artificial intelligence companies, the top three areas of financing accounted for 31% of chip/processor financing 31.5 billion, machine learning application financing 20.7 billion, and natural language processing financing 13.4 billion. The number of chip companies ranked eighth, 33, but the amount of financing is the first, the US chip strength and capital attractiveness can be seen.

China's weakness is in the chip. In recent years, Chinese entrepreneurs and investors have gradually begun to pay attention to chips. As of June 2017, China's processor/chip investment events accounted for the fourth, accounting for 7.55%, but probably due to the foundation. There are fewer companies in the company and the investment threshold is high, resulting in a large gap between the number of incidents and the United States.

The big investment hotspots in the United States are in machine learning applications, and this area is also second only to the chip sucking gold field. American AI has had a collateral effect in all walks of life. China only uses a lot of applications in the fields of autonomous driving/assisted driving, computer vision and images, and it is relatively narrow.

The bubble is about to appear, and the main signals are two:

First, there are more funds and fewer projects

Based on past data and the first half of 2017, the number of new companies in the United States will fall to the bottom this year. It is expected that the number of new companies in the United States will fall between 25-30 before the end of 2017. At the same time, the cumulative financing of the United States continues to grow rapidly, and will eventually stabilize in the range of 138-150 billion yuan. After 18 years, the growth of the number of AI companies in China and the United States will recover, but it will remain flat.

Second, the cycle is long and the revenue is difficult

In layman's terms, artificial intelligence is now overrated. Deep learning originated from neural network research in the 1980s and 1990s. In many cases, cutting-edge research consists of minor modifications and improvements to existing methods that have been designed for decades.

Despite this, the maturity of market-based artificial intelligence technologies and products is still limited. Many projects and technologies are not directly accessible to consumers, and it takes a long time to mature.

Under this premise, entrepreneurial projects have to abandon the mass consumer market and work to solve enterprise-level problems. The innovative company's business model returns to the role of similar traditional IT vendors, further increasing the difficulty of revenue.

It is estimated that by 2020, the cumulative number of AI companies in the United States will exceed 1,200, and the accumulated financing will reach 200 billion yuan. According to historical data, China has reached a total of 74.5 billion in financing at the end of 2017.

Sino-US AI giant card position warThe technical competition that leads the development of the AI ​​industry is mainly the struggle between the giants. At present, Apple, Google, Microsoft, Amazon, and Facebook are all deploying more resources in the field of artificial intelligence; not only foreign giants, but also domestic BAT are full of horsepower and actively deploying artificial intelligence.

The giants of the United States will seize the talents through acquisitions and strengthen their technological reserves. At the same time, they will compete for open source and build an ecosystem. The platform and cloud of artificial intelligence will become the trend of global development. The giants in China, with their advantages in scenes and data, have the strength to compete with American giants in the fields of computer vision and speech recognition.

Industrial layout of Chinese and American giantsThe American giants have the characteristics of an all-industry layout, including the basic layer, the technical layer, and the application layer, all of which have layouts; while the Chinese giants are mainly concentrated on the application side, with only breakthroughs in the technical layer.

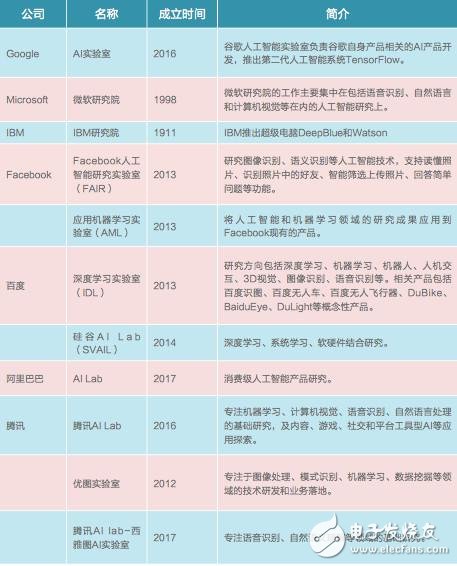

The giants accelerated the research and development of key technologies by recruiting high-end talents and setting up laboratories. Facebook started the Facebook artificial intelligence research laboratory in 2013 to study artificial intelligence technologies such as image recognition and semantic recognition. In the same year, domestic giants Baidu also established a deep learning laboratory, which includes deep learning, computer vision, and robotics.

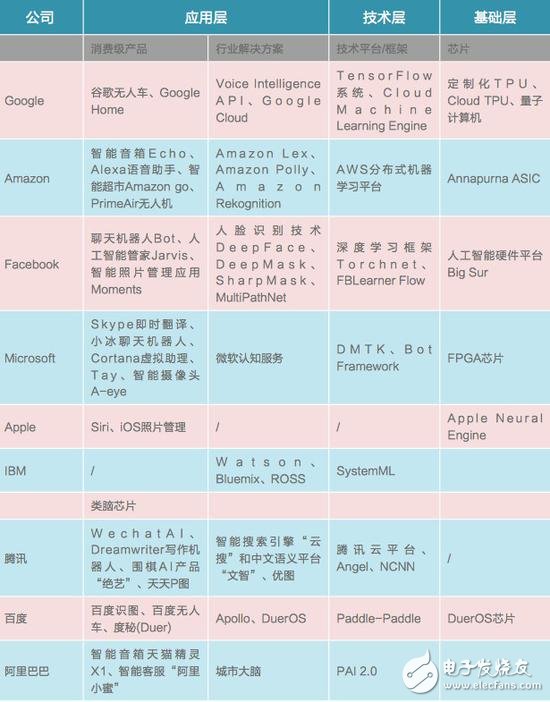

The following figure summarizes the names, year of establishment, and introduction of the AI ​​Labs of the major players:

In addition to setting up laboratories, giants will invest in talent and technology to develop talent and technology through investment and mergers and acquisitions. Among them, Google acquired Deepmind, a deep learning algorithm company, for $400 million in 2014. The AlphaGo developed by the company adds a touch of color to Google's artificial intelligence.

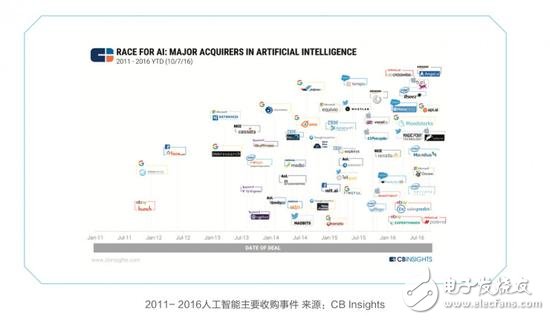

CB Insights' research report compiled the major acquisitions of artificial intelligence from 2011 to 2016. Google has acquired 11 artificial intelligence startups since 2012, the largest among all technology giants. Apple, Facebook and Intel ranked second respectively. Third and fourth. The targets are concentrated in the fields of computer vision, image recognition, and semantic recognition.

There are two reasons why big companies embrace open source: First, build an ecosystem and a moat through open source. Whether Google, Amazon or BAT already have a cloud computing infrastructure, Google, Microsoft has been talking about open source, AWS launched AI features, there is no difference in essence, in order to give their cloud customers more data processing capabilities. In the existing cloud service market, technology giants occupy the majority, and building artificial intelligence-based cloud services will become the next major battleground for the giants. AI is an upgrade of information infrastructure and a huge engine for future industrial development. The giants want to grasp the numerous opportunities that emerged during the upgrade process and empower the industry. Second, open source is an open innovation. Through the open source deep learning platform, not only can attract a large number of developers, but also provide a large amount of data support for machine learning, as well as a large number of real-life scenarios.

Common development frameworks for artificial intelligence include Google's TensorFlow, Facebook's Torch, Microsoft's CNTK, and IBM's SystemML. The status of these frameworks is similar to iOS/Android in the era of artificial intelligence. Open source has also become a common strategy for these software development frameworks.

In 2015, Google brought together in-depth learning technologies to release the second-generation artificial intelligence system TensorFlow and announced its open source. TensorFlow includes a number of frameworks for common deep learning techniques, features and examples.

In 2013, the inventor of convolutional neural network Yann LeCun joined Facebook to lead the company's image recognition technology and natural language processing technology. Facebook's deep learning framework is based on the previous Torch and was open sourced in December 2015. In addition, Facebook has also opened up more than a dozen projects such as the artificial intelligence hardware platform Big Sur.

The domestic giant is also taking the open source route: In 2016, Baidu opened its deep learning platform Paddle-Paddle, covering technologies in the fields of search, image, speech recognition, semantic processing, and user portraits. Different business divisions of Tencent are conducting AI research in different fields. AI Lab focuses on combining technology with Tencent's business scenarios, namely gaming, social, and content ecosystems.

Application layer: robbing the voice interaction portal, campaigning for cloud station servicesRecently, APP analysis company Vetro AnalyTIcs published a report on how AI-based personal assistants reshape user habits. The report shows that with the broad user base of Apple devices, the earliest Siri is still the boss, but lost 15% of users within a year. The opposite is the rise of Amazon Alexa. Alexa was born with the Amazon Echo smart speaker, and the number of users increased by 325% in one year. Google, Microsoft, Apple, and Facebook are all vying for this market. Microsoft also introduced the Invoke speaker with built-in Cortana and the strategy of "ConversaTIon as Platform".

Among domestic enterprises, Jingdong cooperated with Keda Xunfei to deploy smart speakers two years ago, and is committed to becoming a home control center. A few months ago, Ali launched the smart speaker Tmall Elf X1 around the shopping scene. Behind the fierce speaker battle is the battle for the next generation of service portals.

Industry SolutionsArtificial intelligence is bound to move toward cloudization. Machine learning is a key technology for the cloud. It can train large-scale AI networks and continuously learn and improve itself. At this point, Amazon, Google, and other companies with better cloud facilities will have an advantage. Amazon not only builds and optimizes a lot of its own business based on AI, but also leverages AWS Cloud to provide efficient AI solutions for other vendors. "Cloud + AI" has become a new trend, and Google hopes to use AI to catch up with AWS. In 2015, Microsoft released "Microsoft Cognitive Services", a smart API (application programming interface) based on Microsoft's cloud platform Azure, covering five major areas of artificial intelligence technology, including computer vision, voice, language, knowledge. Search for five major APIs.

The domestic BAT Big Three have also introduced artificial intelligence in the field of cloud services.

Baidu began to use GPU instead of CPU for computing two or three years ago to improve data processing capabilities. In 2016, Alibaba Cloud released a new generation HPC platform for deep learning and 3D image rendering. Based on the DI-X deep learning and machine learning platform, Tencent Cloud provides open solutions for image processing, voice processing and natural language processing for multiple scenarios such as autonomous driving, security, smart court, smart home, and intelligent marketing. Committed to "allowing small businesses to use AI capabilities."

Base layer: American giants go deep into the industry core layout chipArtificial intelligence chips mainly include GPUs, FPGAs, ASICs, and brain-like chips. In the era of artificial intelligence, they each exert their advantages and present a state of blossoming.

Google's TPU is specifically designed for its deep learning algorithm Tensor Flow, which is also used in the AlphaGo system. This year's second-generation Cloud TPU theoretical computing power has reached 180T Flops, which can bring significant acceleration to the training and operation of machine learning models.

NVIDIA is the industry leader in GPUs. GPU is the mainstream chip in the field of deep learning, with strong parallel computing power. And another veteran chip giant, Intel is entering the FPGA artificial intelligence chip through a large acquisition. The brain-like chip is an ultra-low-power chip based on neuromorphic engineering and learning from human brain information processing. IBM began to simulate the human brain chip project in 2008.

Apple is developing a dedicated chip called the Apple Neural Engine. The chip is positioned in the local device AI task processing, and AI related tasks such as face recognition and voice recognition are concentrated on the AI ​​module to improve the efficiency of the AI ​​algorithm, and may be embedded in the terminal device of the apple in the future.

Due to the long investment cycle, thick technical barriers and relatively narrow market, the chip is very competitive and difficult to enter.

Who can win the battle of the card position?In the artificial intelligence card position war, the giants tactically converge, that is, to establish technical barriers, the development of software and hardware two lines, to do a good platform ecology. But the strategy is slightly different: Google is the world's largest investment in the field of artificial intelligence and the strongest overall strength. Google hopes to use the open source system to build an AI ecosystem, covering more user usage scenarios, extending from traditional services such as the Internet and mobile Internet to intelligence. Accumulate more data in the fields of home, autopilot, robotics, etc.

Amazon is characterized by the joint efforts of the B and C terminals. Leading the artificial intelligence consumer industry ecosystem with smart speakers and voice assistants. On the other hand, using artificial intelligence to deepen AWS cloud computing services, empowering the entire industry. Facebook's layout in the field of artificial intelligence is centered around the social and social information of its users.

Among the three giants in China, Baidu is relatively radical and announced the “All in AI†strategy. With the strong alliance of Lu Qi, it will fully promote the transformation of Baidu into an AI platform company. Tencent and Ali tested the water based on their own product features.

In addition to positive competition, the giants are actively cooperating in the field of artificial intelligence. In September 2016, Facebook, Amazon, Google, IBM, and Microsoft established the non-profit organization “Partnership on AI†(Artificial Intelligence Cooperation Organization) to share the best technical practices in the AI ​​field and promote public understanding of AI. Excavate the field of AI research that promotes social well-being and provide a platform for open participation.

Sino-US AI talent teamAt present, the competition in the field of artificial intelligence is mainly reflected in the dispute of talents. Only by investing more researchers and continually strengthening basic research will we gain more intelligent technology.

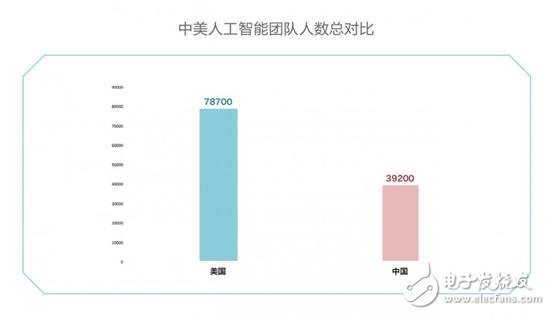

The total amount of industrial talent in the United States is twice that of China.

There are about 78,700 employees in 1078 artificial intelligence companies in the United States, and 39,200 employees in 592 companies in China, only 50% in the United States. Among them, the number of talents in the United States is 13.8 times that of China.

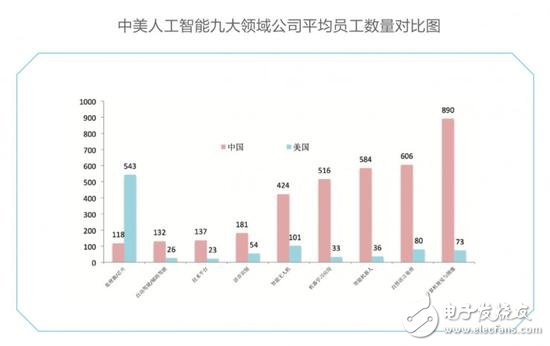

In the field of natural language processing, the number of employees in the United States is three times that of China, 20,200 in the United States and 6,600 in China;

Processor/chip, the number of employees in the United States is 13.8 times that of China, 17900 in the United States, and 1,300 in China;

Machine learning applications, the number of employees in the United States is 1.8 times that of China, 17600 in the United States, and 9,800 in China;

Intelligent drones, the number of employees in the United States is 1.98 times that of China, 9220 in the United States, and 4,660 in China;

Computer vision and images, the number of employees in the United States is 2.87 times that of China, 4335 in the United States, and 1510 in China.

China has only a handful of talents in the field of intelligent robots, 6,400, about three times the number of people in the same field in the United States.

Data company Quid said that last year, technology companies including Google, Facebook, and Microsoft spent about $8.5 billion on research, acquisitions, and talents, four times more than in 2010. Data company Paysa data shows that companies in the United States pay an average of 650 million US dollars per year to 10,000 artificial intelligence personnel. Among them, Amazon spent more than 200 million US dollars to recruit artificial intelligence talents, ranking first among major companies.

There is still a gap between the Chinese and American talent training models. Many colleges and universities do not have artificial intelligence professional for a long time, and in the United States, where artificial intelligence is born, basically large colleges have artificial intelligence majors and research directions. Take Cameroon University as an example, there is a specialized robot research institute, of which there are more than 100 professors of light. In vertical terms, the time for Chinese layout is relatively late. Differences between educational systems will also affect the research focus in the field of artificial intelligence.

At present, the Chinese government is committed to strengthening AI talent development. There is a new trend in the AI ​​talent pool. The “Thousand Talents Program†has attracted a group of outstanding researchers to return to China, and domestic giant companies are also working to attract researchers from all over the world. In the future, it is necessary to continue to establish a core technical personnel training system, strengthen the construction of the first-level discipline of artificial intelligence, strengthen the circulation of talents in enterprises and academia, create a solid talent base, and promote the healthy development of the industry.

Artificial intelligence application hotspotThe artificial intelligence technology has made breakthroughs, especially the perceptual technologies represented by speech recognition, natural language processing, image recognition, and face recognition have made significant technological advances, and a large number of entrepreneurial booms have emerged around these technologies. Related technologies have begun to move from the laboratory to the application market, especially in the fields of transportation, medical, industrial, agricultural, financial, commercial and other fields, which has driven a breakthrough in the development of a number of new technologies, new formats, new models and new products. It has brought about profound industrial changes and is expected to reshape the global industrial landscape.

In the application of this round of artificial intelligence technology, applications such as autonomous driving, intelligent medical care, intelligent security, service robots, intelligent transportation, intelligent manufacturing, and intelligent entertainment have become hotspots in the global artificial intelligence market.

At present, the industrial application of artificial intelligence can be landed, and it can be supported by three major platforms, the open source algorithm platform of the base layer, the technology layer cloud platform, and the application layer. At present, Google, Facebook, and Microsoft have launched an open source platform for deep learning algorithms. Currently, there is only Baidu open platform paddle paddle.

Thanks to the rapid development of China's mobile Internet in recent years, China has accumulated a huge C-end user base, but the traditional industries such as B-side manufacturing, transportation, finance, and medical care are still relatively backward. In contrast, the traditional American industry base. The level of facilities is higher than that of China.

Therefore, the demand for transformation and upgrading of China's traditional industries with artificial intelligence is more urgent, and the stamina for market growth is sufficient.

Domestic artificial intelligence players include Internet giants represented by Baidu, Alibaba and Tencent, as well as AI technology leaders such as Keda Xunfei. These enterprises, as the core strength and key force of domestic artificial intelligence, constitute the first domestic artificial intelligence. An echelon.

The US giant's artificial intelligence applications focus on big data mining. For example, Facebook builds artificial intelligence machines that can understand massive amounts of data. Google has more emphasis on artificial intelligence, including autonomous driving, intelligent robots, and so on. It is more widely used in industry applications.

AutopilotAutomated driving will promote a major technological revolution in the automotive field, so the competition for research and development of smart vehicles in the world is becoming increasingly fierce. At present, the industry is in the stage of assisting driving to semi-automatic driving. Google, Palma University of Italy and Baidu's smart car prototype system, it seems that companies developing R&D cars at home and abroad have put the timeline of unmanned commercials around 2020. Therefore, the next three to four years will be the sprint of the commercialization of this technology.

Most of the intelligent robots are still in the early stage of industrial development, especially the intelligent service robots are still in the initial stage of industrialization. However, as global artificial intelligence is entering the third high tide period, intelligentization has become an important development direction of current robots, artificial intelligence. Innovative integration with robots to further enhance the intelligence of robots. The difference between China and the United States in the field of intelligent robots lies in the fact that the former focuses on the application of robots in professional fields, such as medical, mechanical operations and households; while the latter focuses on smart aids in enterprises or individuals, therefore, the industries involved More, more coverage.

From a global perspective, a large number of intelligent robots such as Japan's ASMO Actroid-F humanoid robot, Pepper intelligent robot, and American BigDog biomimetic robot have emerged rapidly. Giant companies have also acquired intelligent robots as an important carrier of artificial intelligence. Promote the development of artificial intelligence. For example, Google has successively acquired 9 robot companies such as Schaft and Redwood RoboTIcs, and actively deployed in humanoid robot manufacturing and robot coordination. From the perspective of the domestic market, in 2015, the domestic service robot market including commercial robots will be about 8.2 billion yuan. In 2016, it will grow to about 14 billion yuan, and the market size in 2017 will exceed 20 billion yuan. With the growing scale of the intelligent robot market and the wide variety of smart robot entry points, startups and giants have joined the market for intelligent robots from different fields, directions and entry points.

In addition, artificial intelligence is also promising in areas such as smart cities, smart homes, smart finance, smart manufacturing, and smart healthcare. It can liberate a large amount of labor and promote productivity.

Conclusion:In the AI ​​era, the two countries are fully acquainted with each other. China and the United States fully recognize the importance of artificial intelligence and fully support artificial intelligence enterprises from talents to policies. The improvement of national strength comes from the innovation of technology enterprises. The United States is in a leading position with absolute strength, and a number of Chinese start-ups are also gaining momentum, and Chinese companies will also have the opportunity to become the wave of the AI ​​era.

Solar Power Battery,Nife Batteries For Solar,Nickel Iron Battery 400Ah,Ni-Fe Battery 250~400Ah

Henan Xintaihang Power Source Co.,Ltd , https://www.taihangbattery.com