The latest research report of the Shuiqing Muhua Research Center pointed out that in 2010, the LED market scale grew by 58% from $10 billion to $15.8 billion. On the surface, growth is not too much. In fact, driven by the outbreak of LED-TV, the LED market used in LCD TV backlighting has soared from USD 960 million to nearly USD 3.9 billion.

The latest research report of the Shuiqing Muhua Research Center pointed out that in 2010, the LED market scale grew by 58% from $10 billion to $15.8 billion. On the surface, growth is not too much. In fact, driven by the outbreak of LED-TV, the LED market used in LCD TV backlighting has soared from USD 960 million to nearly USD 3.9 billion. LCD TVs with backlights using LEDs reached 26.9% in 2010, and are expected to reach 55.9% in 2011. It is estimated that by 2014 LED will completely replace CCFL. The notebook computer with its backlight using LED was only 59% in 2009 and reached 95% in 2010. Backlight LCDs with LEDs were only 1.5% in 2009 and 15% in 2010, and are expected to reach 40% in 2012.

The global LED industry can be divided into four major regions. First, Europe and the United States, with general lighting as the main attack direction, emphasizing the high reliability and high brightness of products; Second, Japan, the most comprehensive technology, whether it is general lighting or backlight display has the strongest strength, development direction taking into account general lighting, Cars, mobile phones and televisions. Thirdly, in South Korea and Taiwan, notebook computer display backlighting, LED-TV backlighting, and mobile phone backlighting are the main targets, with large shipments, low unit prices, and low gross profit. Fourth, in China, yellow-green light dominates the field of outdoor displays, advertising screens, and credit lights. These applications have low technical requirements for products, low reliability requirements, scattered customers, and small scale. It is usually an engineering project, so the gross profit is not low.

Although mainland China produces 80% of the world's mobile phones, 95% of laptops, 50% of LCD TVs, 95% of LCD monitors, but only production workshops. Key raw materials, small and medium-sized panels, and large-size panels are basically monopolized by Japanese, Korean and Taiwanese companies.

European and American companies also missed the rapidly developing LED backlight market. European and American companies began to target the general lighting market. Although shipments increased a lot in 2010, prices have dropped sharply. These manufacturers have only grown slightly. The greatest growth has been in Japan, South Korea and Taiwan.

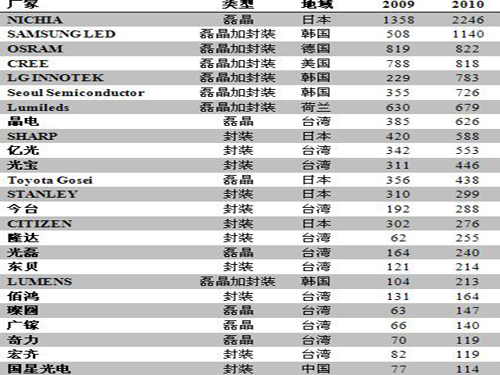

The biggest increase in 2010 was LG INNOTEK, which had revenue of only 229 million U.S. dollars in 2009 and increased to 783 million U.S. dollars in 2010. However, LG INNOTEK sacrificed profits and profit growth was far less than income. Samsung LED revenue also increased a lot, from 508 million US dollars in 2009 to 1.14 billion US dollars, ranking second in the world. Korean company Seoul Semiconductor is also good, revenue increased by 105% to reach 726 million US dollars. Nichia, which ranks first in the world, is also growing at a rapid rate. LED business revenue increased by 65% ​​from 2009 to reach 2.246 billion U.S. dollars. Nichia has ranked first in the world for eight consecutive years since 2003. There are more than 150 LED companies in China, but their total income is less than that of the Nichia Chemicals. The total operating profit is not as good as 40% of Nichia's chemical profits.

2009-2010 Global LED Manufacturer Revenue Statistics (Calculates only LED Epistar and LED Particle Revenue)

Source: Shuiqing Muhua Research Center "2010-2011 Global and China LED Industry Research Report"

China's LED industry has maintained high fever in 2010, and many companies have announced investment of 10 billion yuan. The Chinese government’s eagerness for the upstream of the LED, each MOCVD machine subsidizes 10 million yuan, which has stimulated LED investment frenzy. In 2009, Chinese companies purchased only 25 MOCVD machines and reached 267 in 2010. If we count the number of MOCVD machines purchased by Taiwanese companies on the mainland, it will exceed 400. In 2010, the number of MOCVD machines shipped globally was only 768.

The global MOCVD machine platform is almost monopolized by AIXTRON and VEECO. The frantic investment enthusiasm of Chinese companies has made the two companies make big profits. In 2010, VEECO launched the K465I in the Chinese market, pushing AIXTRON. VEECO's revenue in 2010 increased by 230%.

MOCVD machine is not a car, you can run it after you buy it. MOCVD machines need to be debugged. This process takes 2-4 months for experienced manufacturers. It may be a long time for manufacturers with no experience or technology. Chinese manufacturers have repeatedly promised to dig for Taiwanese talents with a salary of several times. However, taking into account the end of the debugging may be dismissed, LED personnel in Taiwan are rarely moved. Due to lack of talent, the proportion of 267 MOCVDs that were put in place in 2010 was actually not high.

Since the beginning of 2011, due to possible overcapacity and underutilization of MOCVD equipment, some local governments have stopped issuing procurement subsidies for MOCVD equipment.

Led Wall Light,Led Ceiling Light,Smd Led Downlight

Myled Electronics Technology Co., Ltd. , http://www.my-ledlight.com